Artificial Intelligence and Intelligent Analytical Models in the Evaluation of Audit Report Quality: Evidence from the Tehran Stock Exchange

Keywords:

audit report quality; artificial intelligence; intelligent analytical models; random forest; modified audit opinion; Tehran Stock ExchangeAbstract

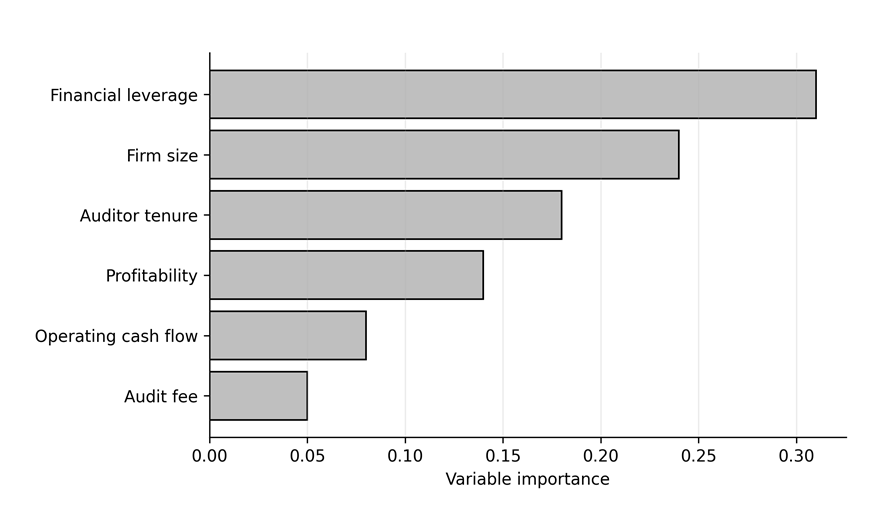

Audit report quality is one of the central mechanisms through which public trust in financial reporting and information transparency in capital markets are strengthened. With the expansion of artificial intelligence and analytical technologies in accounting and auditing, intelligent models provide new opportunities for evaluating audit report quality through data-driven prediction. This study aimed to design and compare intelligent analytical models for evaluating audit report quality among companies listed on the Tehran Stock Exchange. The study used a quantitative empirical design. Audit report quality was operationalized as the issuance of a modified audit opinion. The independent variables included financial leverage, firm size, profitability, auditor tenure, audit fee, operating cash flow ratio. The sample consisted of 150 listed companies over the period 2017–2023. Logistic regression, decision tree, random forest, and gradient boosting models were used to analyze the data. Model performance was evaluated using accuracy, precision, recall, F1-score, and ROC-AUC. The results indicated that financial leverage had a positive and significant association with the probability of receiving a modified audit opinion, whereas firm size, profitability, auditor tenure, and operating cash flow were negatively associated with modified audit opinions. Among the predictive models, random forest achieved the strongest performance (accuracy = 0.83, precision = 0.81, recall = 0.79, and ROC-AUC = 0.88). Variable-importance analysis showed that financial leverage, firm size, auditor tenure, and profitability were the most influential predictors. The findings suggest that intelligent analytical models, particularly random forest, can support audit-risk assessment, regulatory monitoring, and investor decision-making in the Iranian capital market.

Downloads

References

Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big data and analytics in the modern audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-27. https://doi.org/10.2308/ajpt-51684

Breiman, L. (2001). Random forests. Machine Learning, 45(1), 5-32.

Brown-Liburd, H., Issa, H., & Lombardi, D. (2015). Behavioral Implications of Big Data's Impact on Audit Judgment and Decision Making and Future Research Directions. Accounting Horizons, 29(2), 451-468. https://doi.org/10.2308/acch-51023

DeAngelo, L. E. (1981). Auditor size and audit quality. Journal of Accounting and Economics, 3(3), 183-199. https://doi.org/10.1016/0165-4101(81)90002-1

Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management. The Accounting Review, 70(2), 193-225. https://doi.org/10.2308/TAR-9505096112

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of Accounting and Economics, 58(2-3), 275-326. https://doi.org/10.1016/j.jacceco.2014.09.002

Fedyk, A., Hodson, J., Khimich, N., & Fedyk, T. (2022). Is artificial intelligence improving the audit process? Review of Accounting Studies, 27, 938-985. https://doi.org/10.1007/s11142-022-09697-x

Francis, J. R. (2004). What do we know about audit quality? The British Accounting Review, 36(4), 345-368. https://doi.org/10.1016/j.bar.2004.09.003

Francis, J. R., & Yu, M. D. (2009). Big 4 office size and audit quality. The Accounting Review, 84(5), 1521-1552. https://doi.org/10.2308/accr.2009.84.5.1521

Friedman, J. H. (2001). Greedy function approximation: A gradient boosting machine. The Annals of Statistics, 29(5), 1189-1232. https://doi.org/10.1214/aos/1013203451

Geiger, M. A., & Raghunandan, K. (2002). Auditor tenure and audit reporting failures. Auditing: A Journal of Practice & Theory, 21(1), 67-78. https://doi.org/10.2308/aud.2002.21.1.67

Hastie, T., Tibshirani, R., & Friedman, J. (2009). The elements of statistical learning: Data mining, inference, and prediction (2nd ed.). Springer. https://doi.org/10.1007/978-0-387-84858-7

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

Kokina, J., & Davenport, T. H. (2017). The emergence of artificial intelligence: How automation is changing auditing. Journal of Emerging Technologies in Accounting, 14(1), 115-122. https://doi.org/10.2308/jeta-51730

Myers, J. N., Myers, L. A., & Omer, T. C. (2003). Exploring the term of the auditor-client relationship and the quality of earnings: A case for mandatory auditor rotation? The Accounting Review, 78(3), 779-799. https://doi.org/10.2308/accr.2003.78.3.779

Palmrose, Z. V. (1988). An analysis of auditor litigation and audit service quality. The Accounting Review, 63(1), 55-73. https://doi.org/10.2308/TAR-4482234

Perols, J. (2011). Financial statement fraud detection: An analysis of statistical and machine learning algorithms. Auditing: A Journal of Practice & Theory, 30(2), 19-50. https://doi.org/10.2308/ajpt-50009

Simunic, D. A. (1980). The pricing of audit services: Theory and evidence. Journal of Accounting Research, 18(1), 161-190. https://doi.org/10.2307/2490397

Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355-374. https://doi.org/10.2307/1882010

Sutton, S. G., Holt, M., & Arnold, V. (2016). The reports of my death are greatly exaggerated: Artificial intelligence research in accounting. International Journal of Accounting Information Systems, 22, 60-73. https://doi.org/10.1016/j.accinf.2016.07.005

Downloads

Publication Timeline

- Submitted

- Revised

- Accepted