Development of a Social Value Framework Based on Strategic Management with a Stakeholder Theory Approach Using Qualitative Thematic Analysis

DOI:

https://doi.org/10.61838/kman.ijimob.5099Keywords:

Social value, strategic management, stakeholder theory approach, implementation structures.Abstract

Objective: The objective of this study was to develop and conceptualize an integrated framework for social value grounded in strategic management principles through the lens of stakeholder theory.

Methods and Materials: This research was conducted as an exploratory qualitative study within an interpretive paradigm using thematic analysis as the primary methodological approach. The study population consisted of academic and professional experts in accounting, financial reporting, sustainability standards, and corporate governance, selected through purposive and snowball sampling. Data were collected through documentary analysis of relevant scholarly texts and semi-structured interviews with fourteen experts until theoretical saturation was achieved. Interviews were audio-recorded, transcribed verbatim, and analyzed following the systematic procedure of thematic analysis and thematic network construction. Trustworthiness was ensured through prolonged engagement, member clarification during interviews, researcher triangulation, and inter-coder agreement assessment. The analysis aimed to identify patterns of meaning leading to the extraction of basic, organizing, and global themes forming the conceptual structure of the proposed framework.

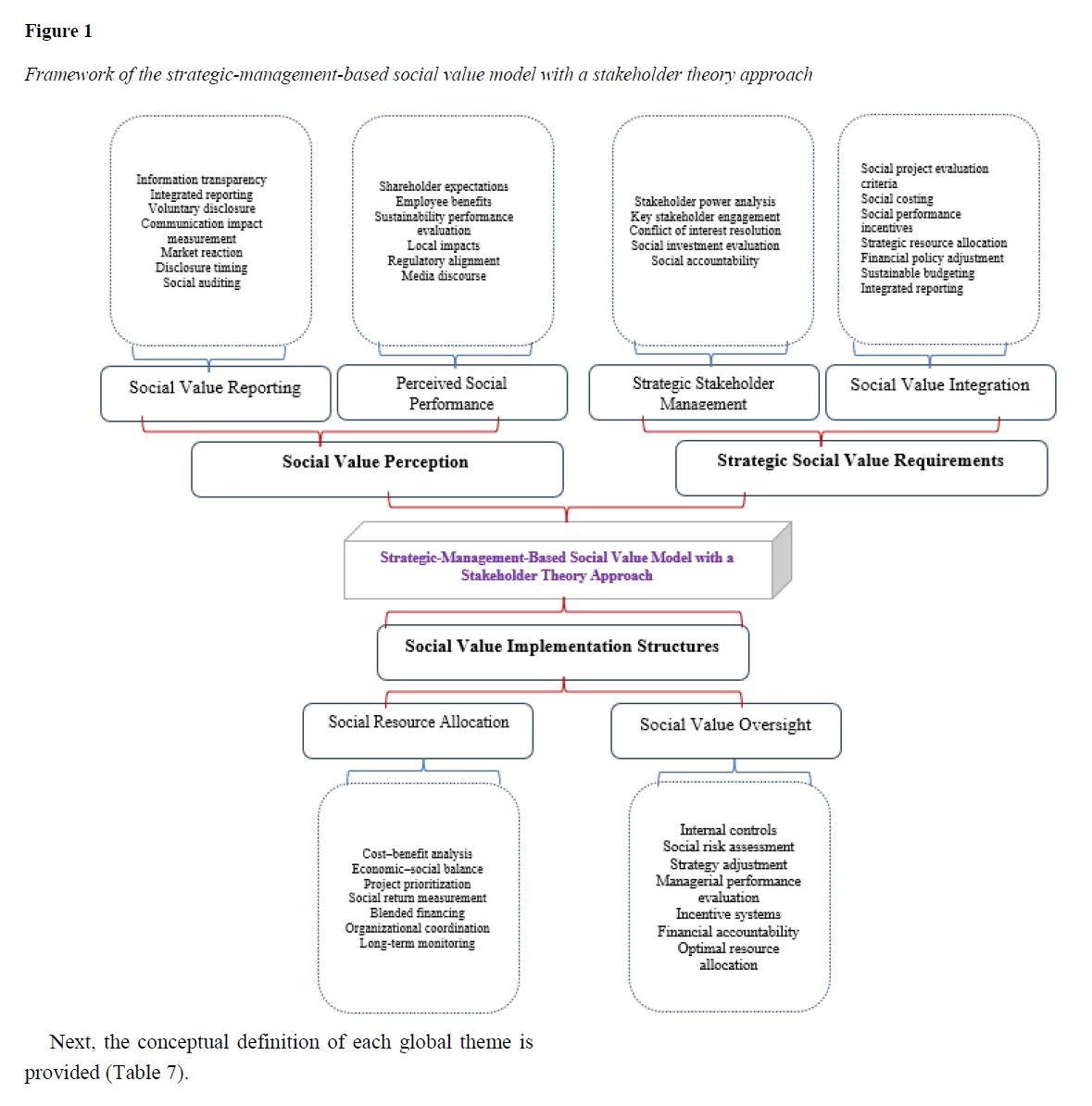

Findings: The inferential analysis revealed a coherent multidimensional structure of social value consisting of three interrelated global themes: strategic requirements of social value, social value perception, and social value implementation structures. These dimensions collectively demonstrate that social value operates as a strategic organizational capability rather than a peripheral ethical activity. The findings indicate that effective integration of social value depends on alignment between strategic decision-making, stakeholder management mechanisms, performance perception processes, and organizational execution systems. The thematic relationships further suggest that organizations generate sustainable social value when governance structures, performance evaluation practices, and resource allocation mechanisms are systematically aligned with stakeholder expectations and long-term strategic objectives.

Conclusion: The study concludes that embedding social value within strategic management requires a holistic organizational architecture that integrates stakeholder engagement, strategic governance, perception management, and operational execution mechanisms. The proposed framework offers a theoretically grounded and practically applicable model for transforming social value from a normative concept into an institutionalized strategic process capable of enhancing organizational legitimacy, sustainability performance, and stakeholder trust.

Downloads

References

Amoako, G. K., Adam, A. M., Tackie, G., & Arthur, C. L. (2021). Environmental accountability practices of environmentally sensitive firms in Ghana: Does institutional isomorphism matter? Sustainability, 13(3), 122-141. https://doi.org/10.3390/su1303122

Ansari Nik, S., & Tabibi, S. J. (2025). A behavioral approach to the role of stakeholders in the corporate governance model of the Social Security Organization of Iran and its affiliated companies. Public Administration, 17(1), 221-256. https://jipa.ut.ac.ir/article_101072.html

Bansal, S., Garg, I., & Singh, S. (2023). Corporate social responsibility: insights from COVID‐19 and stakeholder theory. Global Business and Organizational Excellence, 42(6), 154-169. https://doi.org/10.1002/joe.22222

Bonnafous-Boucher, M., & Rendtorff, J. D. (2016). Stakeholder theory: A model for strategic management. Springer. https://doi.org/10.1007/978-3-319-44356-0

Córdova-Aguirre, L. J., & Ramón-Jerónimo, J. M. (2024). Designing a sustainability assessment framework for Peruvian manufacturing small and medium enterprises applying the stakeholder theory approach. Sustainability, 16(5), 1853. https://doi.org/10.3390/su16051853

Dagestani, A. A., Alnafrah, I., Smutka, L., Bilan, Y., & Chen, P. (2024). Greenwashing and stakeholder theory in China: an empirical evidence of corporate social responsibility and firms performance. Environment, Development and Sustainability, 1-26. https://doi.org/10.1007/s10668-024-04849-2

Esposito, P., Marrone, A., Pontrelli, V., & Rella, A. (2025). Exploring drivers and factors of benefit impact reports quality: Retracing a stakeholder theory approach. Business Strategy and the Environment, 34(1), 555-569. https://doi.org/10.1002/bse.3974

Farahi, M., & Akbarpour, H. (2022). Investigating the relationship between sustainable environmental performance reporting and the cost of debt financing: Examining the effects of corporate reputation. Scientific Journal of New Research Approaches in Management and Accounting, 6(22), 880-896. https://majournal.ir/index.php/ma/article/view/1611

Faraji, O., Jannati Daryakenari, F., Mansouri, K., & Younesi Moti, F. (2020). Social responsibility and firm value: The moderating role of earnings management. Scientific Journal of Social Capital Management, 7(1), 25-58. https://jscm.ut.ac.ir/article_71593.html

Gring-Pemble, L., Unruh, G., & Shaked, E. (2025). Implementing a stakeholder capitalism approach through values-based leadership: case studies in the private, nonprofit and educational sectors. Corporate Governance: The International Journal of Business in Society, 25(1), 31-46. https://doi.org/10.1108/CG-03-2023-0110

Hajializadeh, S., Khajeh Hassani, M., & Amiri, A. (2020). Investigating the relationship between stakeholder theory, corporate social responsibility and financial performance. Scientific Journal of New Research Approaches in Management and Accounting, 4(15), 92-102. https://majournal.ir/index.php/ma/article/view/636

Jasper, A., Sepich, N. C., Gilbert, S. B., Kelly, J. W., & Dorneich, M. C. (2023). Predicting cybersickness using individual and task characteristics. Computers in human Behavior, 14(6), 124-141. https://doi.org/10.1016/j.chb.2023.107800

Johnson, R., & Smith, L. (2023). The impact of green accounting standards on organizational performance. Sustainability Accounting, Management and Policy Journal, 14(2), 123-140. https://doi.org/10.1108/SAMPJ-01-2022-0034

Jones, T. M., Harrison, J. S., & Felps, W. (2018). How applying instrumental stakeholder theory can provide sustainable competitive advantage. Academy of Management Review, 43(3), 371-391. https://doi.org/10.5465/amr.2016.0111

Khalili, M., Zabihi, A., & Faghani Makarani, K. (2024). Presenting a model for the impact of organizational culture and contingency factors on sustainability reporting with an economic performance approach (GRI201). Journal of Management Accounting and Auditing Knowledge, 13(50), 319-338. https://www.jmaak.ir/article_22277.html

Langazel, T. (2017). Strategic intelligence in social impact assessment. Long Range Planning, 50(5), 621-635. https://doi.org/10.1016/j.lrp.2016.11.002

Mahmoudi, R., Talebnia, G., Vakilifard, H., Ahmadi, F., & Moradi Shadadi, K. (2023). Presenting a sustainability reporting model based on the grounded theory approach in companies listed on the Tehran Stock Exchange. Financial Economics, 17(64), 207-222. https://www.sid.ir/paper/1097915/fa

Mansour, G., Poursoleiman, E., Homayoun, S., Rezaei, Z., & Rezaee, Z. (2022). Business sustainability performance and corporate financial performance: The mediating role of optimal investment. Managerial Finance, Advance online publication. https://doi.org/10.1108/MF-01-2021-0040

Mu, H. L., Xu, J., & Chen, S. (2024). The impact of corporate social responsibility types on happiness management: a stakeholder theory perspective. Management Decision, 62(2), 591-613. https://doi.org/10.1108/MD-02-2023-0267

Pies, I., & Valentinov, V. (2024). Trade-offs in stakeholder theory: an ordonomic perspective. Social Responsibility Journal, 20(5), 975-997. https://doi.org/10.1108/SRJ-06-2023-0321

Robb, C. C., Brownell, K. M., Brännback, M., & Rumi, S. (2025). Applying resource-based theory to social value creation: A conceptual model of contributive advantage. Journal of Small Business Management, 63(1), 147-169. https://doi.org/10.1080/00472778.2024.2309498

Shah, M. U., & Guild, P. D. (2022). Stakeholder engagement strategy of technology firms: A review and applied view of stakeholder theory. Technovation, 114, 102460. https://doi.org/10.1016/j.technovation.2022.102460

Downloads

Additional Files

Publication Timeline

- Submitted

- Revised

- Accepted