The Impact of Audit Firm Rankings on Firm Reputation and Size

Keywords:

Audit firm rankings, firm reputation, firm size, audit quality, internal resources, stock exchange ranking, community ranking, municipality rankingAbstract

Objective: Audit firm rankings are widely regarded as indicators of quality and reliability, influencing both the reputation and size of audit firms. This study aims to examine the impact of audit firm rankings on the reputation and size of audit firms, providing insights into how these rankings shape client perceptions and operational scale.

Methodology: This quantitative study analyzes data from 1171 audit firms. Key variables include audit firm rankings from community, stock exchange, and municipality sources, as well as firm size, number of partners, certified public accountants (CPAs), professional staff, and administrative staff. Descriptive statistics and multiple regression analyses were used to explore the relationships between rankings, firm size, and reputation.

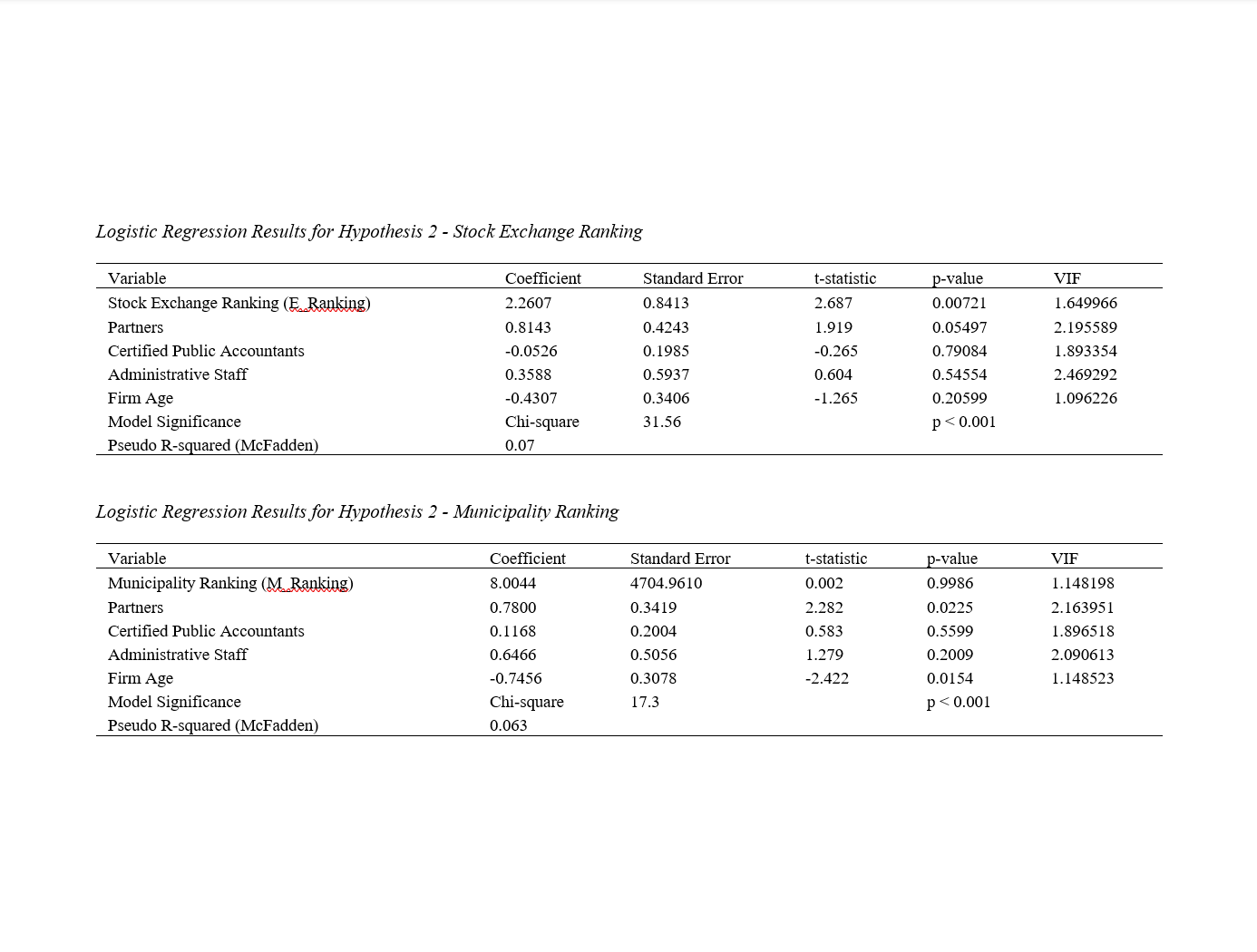

Findings: Descriptive statistics revealed significant variability in audit firm rankings and firm sizes. Multiple regression analyses indicated that audit firm rankings did not significantly impact firm size. However, the number of partners and administrative staff were significant predictors of firm size. Logistic regression results showed that stock exchange rankings significantly influenced firm reputation, while community and municipality rankings did not. The number of administrative staff and firm age also played roles in shaping reputation.

Conclusion: The study concludes that internal characteristics, such as the number of partners and administrative staff, are critical determinants of audit firm size and reputation. While stock exchange rankings significantly influence reputation, other ranking sources are less impactful. Audit firms should focus on enhancing their internal resources and operational efficiency to improve their market position and client perceptions.

Downloads

Downloads

Additional Files

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2024 Arsalan Esmaeli Kakroudi (Author); Yosuf Taghipouryani gilani (Corresponding Author); Mohammadreza Pourali, Razieh Alikhani (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

How to Cite