Identification and Ranking of Financial, Non-Financial, and Behavioral Components Influencing Earnings Response Coefficient in the Iranian Capital Market (Data Mining Approach)

DOI:

https://doi.org/10.61838/kman.ijimob.4.4.14Abstract

Objective: The relationship between accounting profit and investor reactions, as well as stock price changes, is measured using the Earnings Response Coefficient (ERC). Previous research indicates a variation in ERC between companies and over time, which is attributed to specific company factors and characteristics. The aim of this study is to identify and rank the financial, non-financial, and behavioral components affecting companies' ERC.

Methodology: Using data from 153 companies listed on the Tehran Stock Exchange over the period 2013 to 2022, and employing data mining techniques and two methods: stepwise forward regression and regression decision tree, the influential components on ERC were identified and ranked.

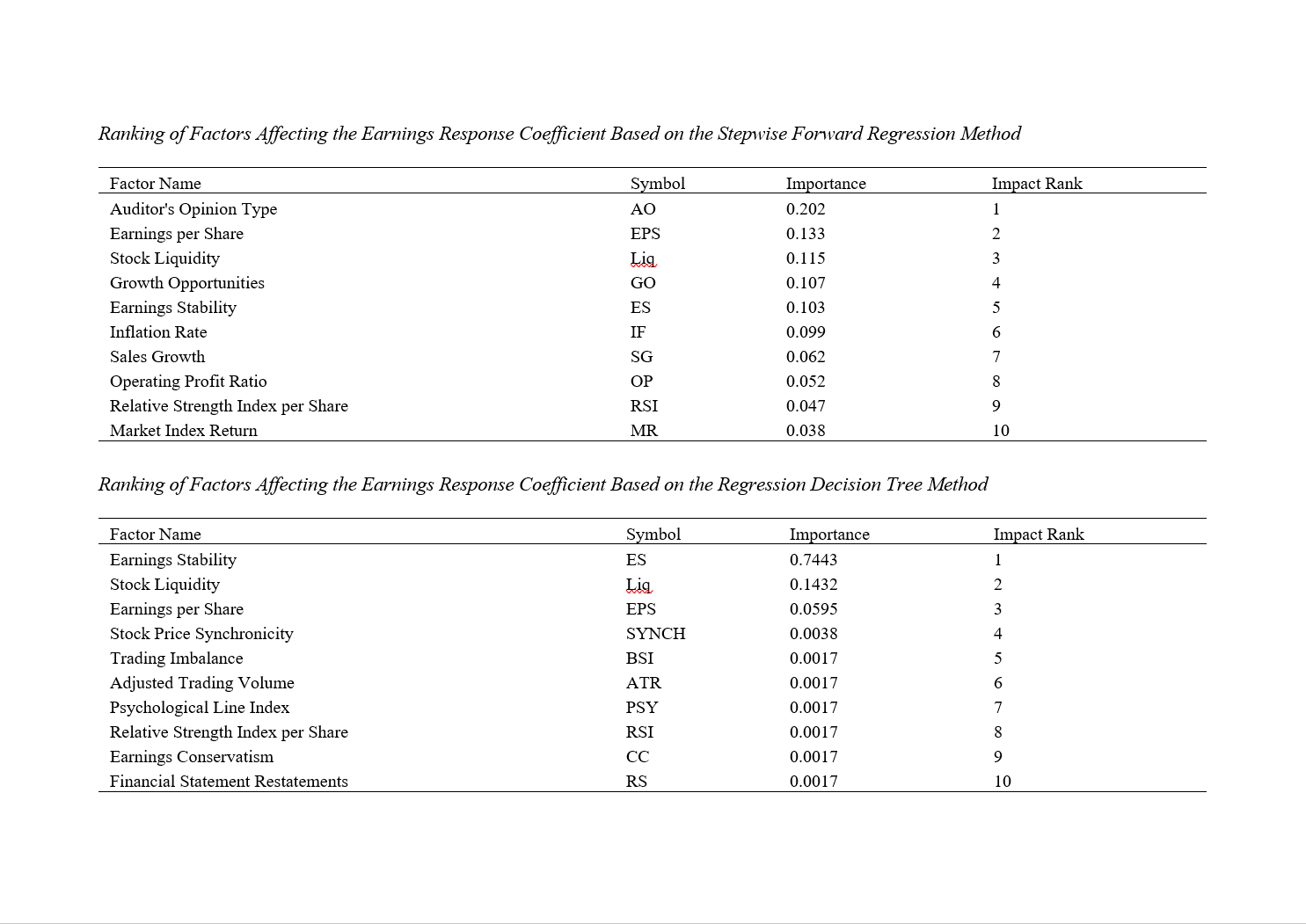

Findings: The results of the stepwise forward regression method indicated that the components of auditor's opinion type, earnings per share (EPS), stock liquidity, growth opportunities, earnings stability, inflation rate, sales growth, operating profit ratio, relative strength index per share, and market index return respectively influence ERC. The regression decision tree method results also showed that the components of earnings stability, stock liquidity, EPS, stock price synchronicity, stock trading imbalance, adjusted trading volume, psychological line index, relative strength index per share, earnings conservatism, and financial statement restatements respectively influence ERC. The Wilcoxon test results also showed that the ranking of components influencing ERC is not the same in the two methods. Additionally, comparing the mean absolute error of the two methods indicated that the regression decision tree method identifies and ranks the influential components on ERC more accurately.

Conclusion: The results of both methods confirm the high impact of EPS, stock liquidity, earnings stability, and relative strength index per share on the ERC of companies.

Downloads

Downloads

Additional Files

Publication Timeline

Issue

Section

License

Copyright (c) 2024 Mansour Moghadasi (Author); Alireza Ghiasvand (Corresponding Author); Farid Sefati (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.