Examination of the Role of Ethics-Based Auditing in the Development of Trustworthy Artificial Intelligence (Case Study: Auditing Firms in Tehran)

DOI:

https://doi.org/10.61838/kman.ijimob.4.4.27Keywords:

Auditing, Ethics-Based Auditing, Artificial Intelligence, TrustAbstract

Objective: The study aims to examine the role of ethics-based auditing in the development of trustworthy artificial intelligence (AI) within auditing firms based in Tehran.

Methodology: The research is applied in its objective and descriptive-survey in its execution. The study utilizes thematic content analysis to identify the necessity and importance of the research. A meta-analysis is conducted to review the literature. In-depth interviews with experts were carried out until theoretical saturation was achieved, followed by data coding. The model was tested using structural-interpretive equations and a questionnaire as tools to apply the research findings to the studied population. The sample includes managers of auditing firms in Tehran, selected using the snowball sampling method. Data were collected using both open and closed questionnaires and structured interviews.

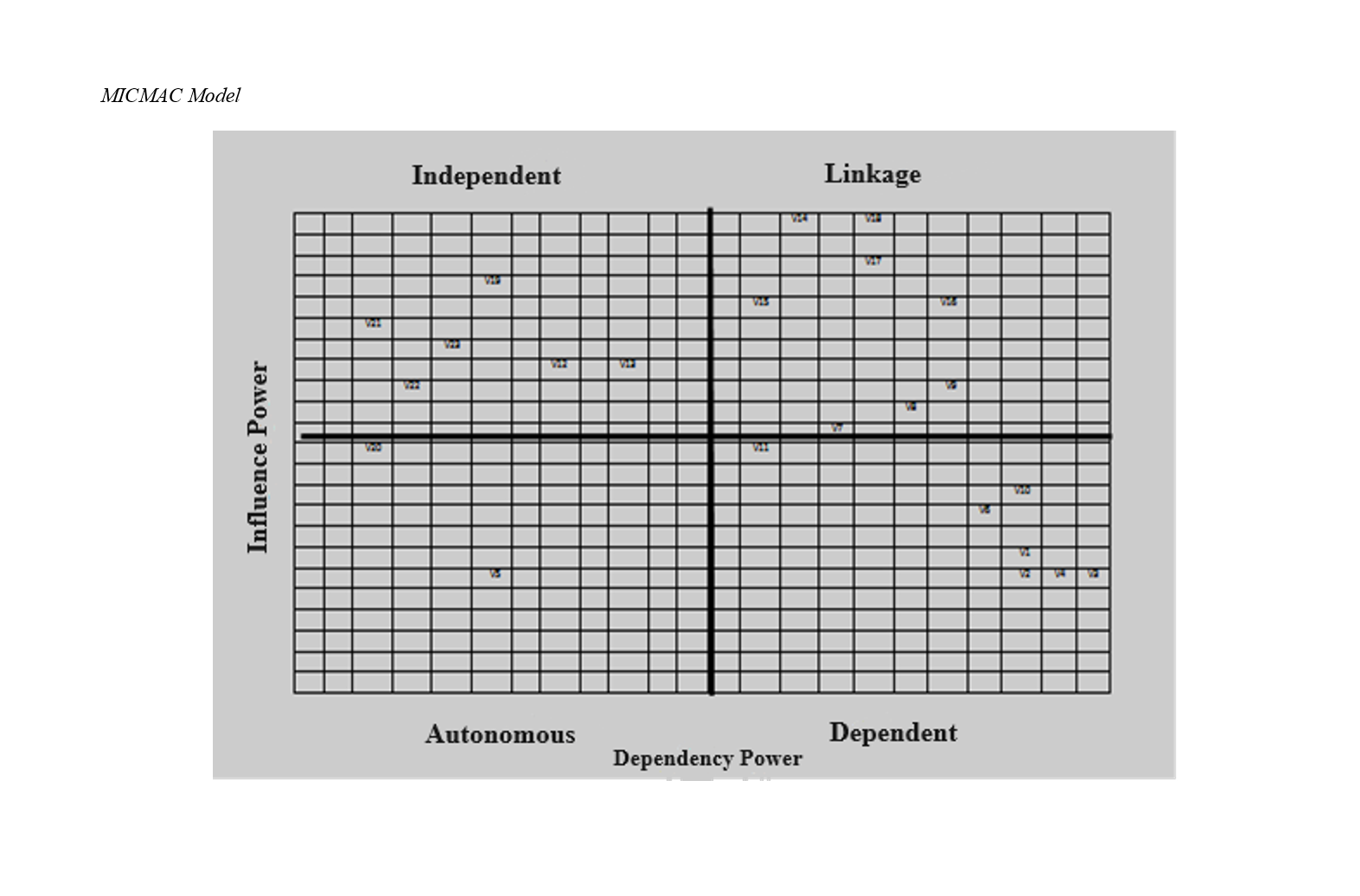

Findings: The study identified 14 key indicators of ethics-based auditing influencing the development of trustworthy AI, including technical issues, organizational complexity, legal issues, increased transparency, reduced information asymmetry, stakeholder participation and cooperation, decentralization, ease of traceability, trustworthiness, infrastructure, real-time accounting, audit data security, flexibility, and cybersecurity. These indicators were categorized into four groups based on their influence power and dependency: independent, linkage, autonomous, and dependent variables.

Conclusion: The findings suggest that ethics-based auditing can significantly influence the development of trustworthy AI in auditing firms. From an agency theory perspective, blockchain technology and AI increase the difficulty of data manipulation and enhance process automation, improving transparency and reducing fraud. From a stakeholder theory perspective, blockchain technology promotes an open and inclusive environment, enhancing collaboration and business opportunities. The integration of blockchain and AI in accounting practices can meet the diverse needs of different users, improving trust and reliability in financial reporting.

Downloads

Downloads

Additional Files

Publication Timeline

- Submitted

- Revised

- Accepted

Issue

Section

License

Copyright (c) 2024 Fariba Habibikilak (Corresponding Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.