Presenting A Model for Identifying Personality and Ethical Characteristics of Independent Auditors in Iran

DOI:

https://doi.org/10.61838/kman.ijimob.4.2.29Keywords:

Personality Characteristics, Ethical Characteristics of Auditors, Openness, Conscientiousness, ExtraversionAbstract

Objective: The aim of the present research is to propose a model for identifying personality and ethical characteristics of independent auditors in Iran.

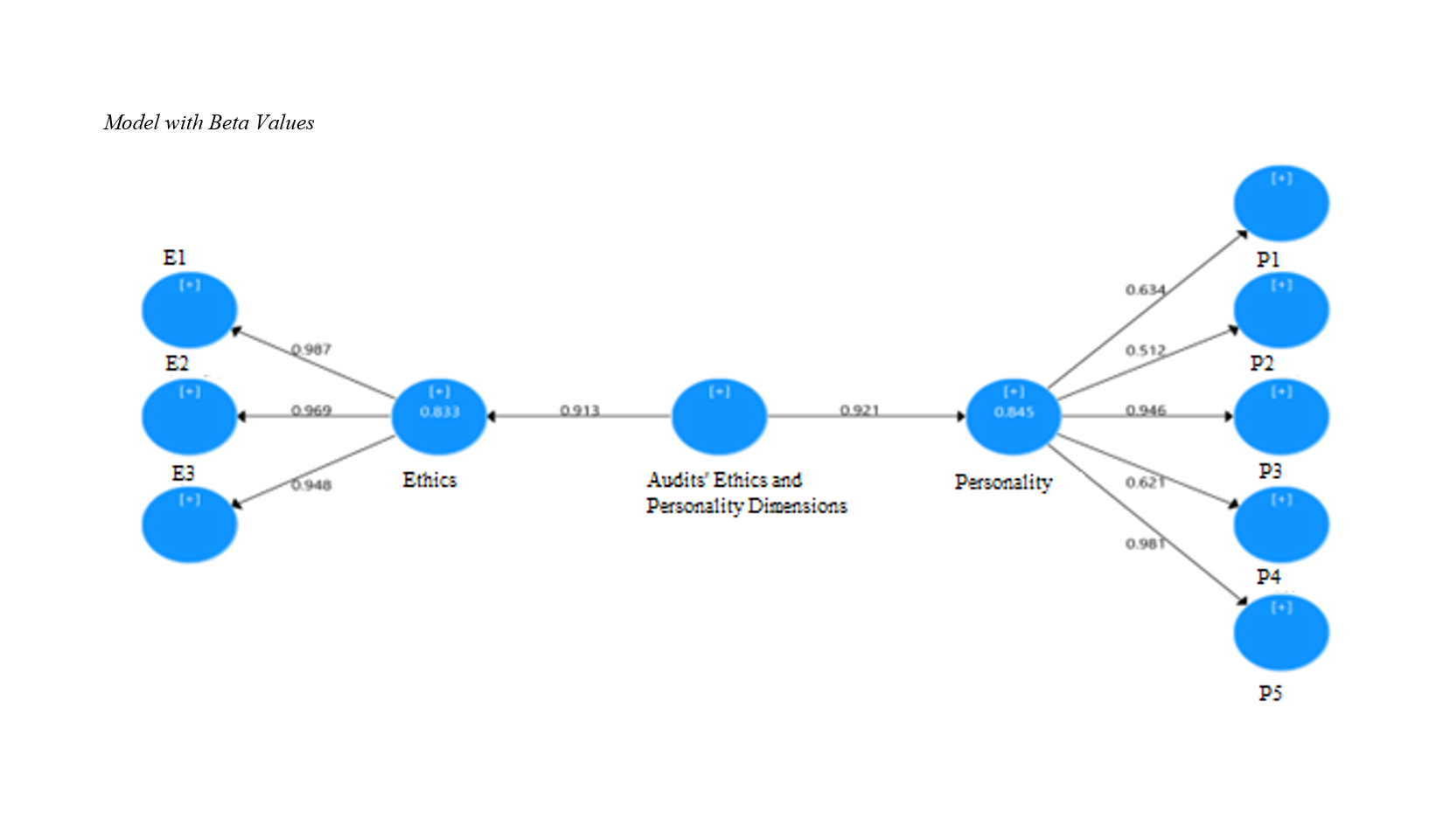

Methodology: The research method, considering its objective, is applied and mixed (qualitative-quantitative) in terms of execution. The qualitative sample includes 10 participants consisting of academic experts and auditors (faculty members in the field of auditing and experienced auditors), selected purposively, and the quantitative sample includes 2700 auditors in five provinces including Tehran, Mashhad, Tabriz, Isfahan, and Mazandaran. According to Cochran's formula, 336 individuals were selected as samples in these 5 provinces, initially selected cluster-wise and then randomly in each province. Data collection in the qualitative section was done using semi-structured interviews with members of the statistical community, and in the quantitative section, it was carried out through a researcher-made questionnaire. Data analysis in the qualitative section was performed using thematic analysis method (basic themes, organizing, and overarching themes), and the process of coding and textual analysis of interviews was done in MAXQDA 2018 software. In the quantitative section, SPSS 16 and Smart PLS software were used, and inferential analysis was performed using the factor analysis method.

Findings: The results in the qualitative section showed that the ethical dimension includes (individual aspect, organizational aspect, environmental aspect) and the personality dimension includes (openness, conscientiousness, extraversion, agreeableness, neuroticism). Based on the results of the quantitative analysis, the model was confirmed, and the relationships between the model variables were found to be significant with a strong fit.

Conclusion: Based on the results of this study, it is recommended that when hiring auditors to improve auditors' ethical performance, their personality traits be examined based on personality tests, and the importance of the subject be explained to them by holding training courses at the time of entry into the auditing profession.

Downloads

Downloads

Additional Files

Publication Timeline

Issue

Section

License

Copyright (c) 2024 Saeid Goodarzi (Author); Mahmoud Hematfar (Corresponding Author); Mohammadhasan Janani (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.