Phenomenology of Management Accounting from the Perspective of the Board of Directors

Abstract

Objective: This study aims to phenomenologically explore management accounting from the perspective of the board of directors to understand its fundamental categories and challenges in organizational contexts.

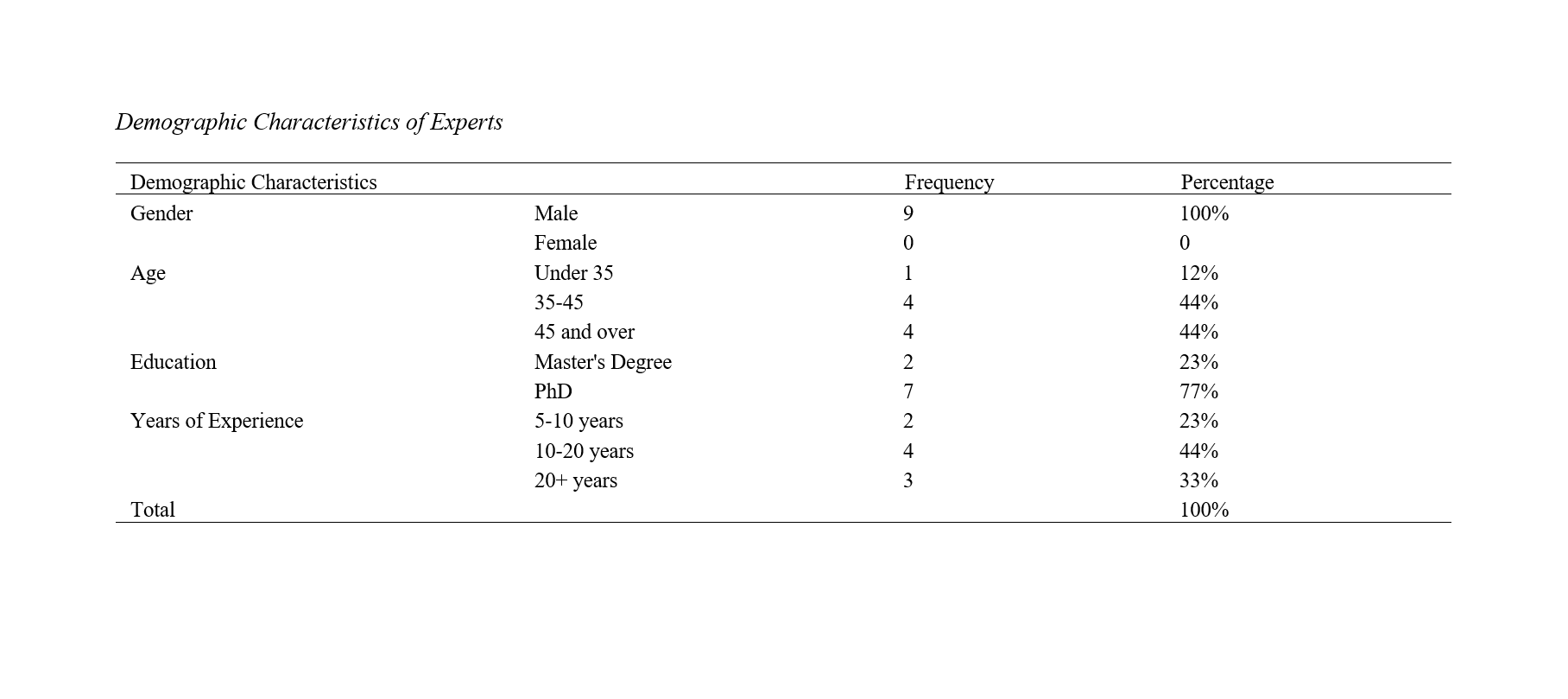

Methodology: This qualitative study adopts an interpretive philosophy and employs an inductive approach. Data were collected through semi-structured interviews with nine board members, selected using purposive snowball sampling until theoretical saturation was achieved. Colaizzi's seven-step method was applied for thematic analysis, supported by MAXQDA 20 software.

Findings: The analysis identified 91 subcategories grouped into nine main themes: organizational culture, individual characteristics of accountants, understanding the company’s historical and future performance, monitoring operational decisions, comprehensive management performance evaluation, modern management strategies, challenges in management accounting, roles of the management accounting unit, and identifying opportunities for operational improvement.

Conclusion: The research highlights the importance of management accounting as a strategic tool for enhancing decision-making, accountability, and organizational efficiency. Recommendations emphasize fostering an adaptive organizational culture, enhancing the skills of accountants, addressing structural challenges, and leveraging modern management strategies to optimize the role of management accounting in corporate governance and decision-making.

Downloads

Downloads

Additional Files

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2024 Hossein Haghshenas, Ali Ebrahimi Kordlar, Ezatollah Abbasian (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

How to Cite