Development of a Comprehensive Continuous Auditing Model for Risk Management in Iranian Commercial Banks

DOI:

https://doi.org/10.61838/kman.ijimob.5217Keywords:

Continuous auditing, risk management, Iranian commercial banks, grounded theory, structural equation modelingAbstract

Objective: The present study aimed to develop a comprehensive continuous auditing model with a focus on risk management in Iranian commercial banks.

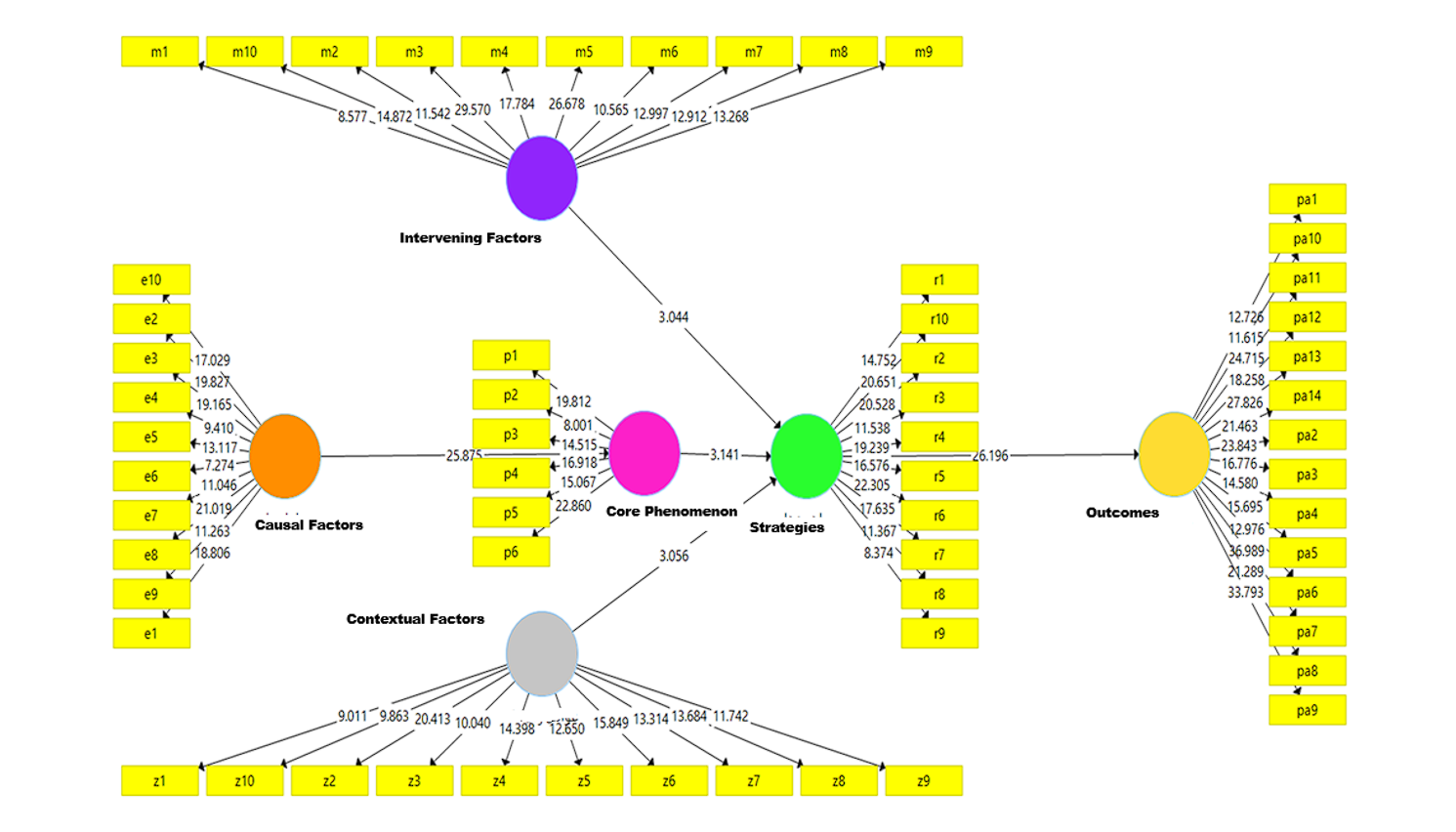

Methods and Materials: This study employed a mixed-methods design (qualitative–quantitative). In the qualitative phase, the grounded theory approach based on Anselm Strauss and Juliet Corbin was utilized, while the quantitative phase complemented the analysis. The statistical population in the qualitative section consisted of 22 banking experts, including managers and heads of internal audit departments from Tejarat, Mellat, and Saderat banks, as well as academic specialists, who were selected through snowball sampling. In the quantitative section, the sample size was determined purposively and included 146 senior managers from the aforementioned banks in East Azerbaijan Province. Data collection tools included structured interviews (qualitative) and a questionnaire developed based on the qualitative model (quantitative). Data analysis in the qualitative phase was conducted using three-stage coding (open, axial, and selective coding), and in the quantitative phase through structural equation modeling (SEM) using SmartPLS version 3.1.1.

Findings: Qualitative analysis led to the development of a six-dimensional conceptual model, including causal conditions (risk identification and assessment, controls, and assurance), contextual conditions (infrastructure, human resources, and culture), intervening conditions (complexity, rate of change, data, security, and cost), the core phenomenon (continuous auditing with a focus on risk management), strategies (managerial, technological, and structural), and outcomes (risk reduction and managerial development). The results of the quantitative phase confirmed a good model fit and revealed significant relationships among the model dimensions; in particular, a strong and statistically significant relationship was observed between causal conditions and the core phenomenon, as well as between the core phenomenon and strategies, at a high confidence level.

Conclusion: The findings indicate that the successful implementation of continuous auditing and the achievement of optimal risk management in Iranian commercial banks require the identification and strengthening of enabling factors, proactive management of challenges, and the application of comprehensive strategies (managerial, technological, and structural). The proposed model provides an effective framework for enhancing supervision and promoting managerial development within the country’s banking system.

Downloads

References

Asgarnezhad Nouri, B., Zarei, G., & Beigi Firouzi, A. (2022). The impact of risk management on new product development in the banking industry. Quarterly Journal of Public Management Research, 15(58), 289-316.

Attaf, W. F., & Bensbahou, A. (2025). The impact of risk-based internal audit approach on improving risk management processes: A field study in Yemeni Islamic banks (Aden). Journal of Management World, 1, 180-190. https://doi.org/10.53935/jomw.v2024i4.634

Bayati, G., Mohammadpour Zarandi, M. E., Kordlouie, H. R., & Fadavi, A. (2024). Designing a mathematical algorithm for optimizing banks' foreign exchange asset portfolios based on fuzzy logic and related risk indicators (Case study: Bank Mellat). Investment Knowledge, 13(50), 39-72.

Beikzadeh Abbasi, F. (2024). Comprehensive risk management model (Case study: Pharmaceutical industry). Investment Knowledge, 13(50), 73-93.

Ezzati Jadidi, M. (2022). Investigating the short-term and long-term impact of internal controls and risk management on cash assets of selected companies listed on the Tehran Stock Exchange. Civilica.

Khodabakhshi Gorgani, F., Ziaei, M., Taghavifard, M. T., & Torkestani, M. S. (2022). A model for risk management in the hotel industry. Quarterly Journal of Tourism Management Studies, 17(57), 39-71.

Manafi Sharafabad, G. (2022). Presenting a theoretical framework for project risk management plan. Journal of Science and Engineering Elites, 7(3).

Mogharrab, A., Gerami, A., & Mousavi, Z. S. (2021). The concept of risk and its application in the capital market. 9th International Conference on Management and Humanities Research in Iran, Tehran, Iran.

Mortazavi, S. M., & Shokrkhah, J. (2022). Identifying the weaknesses of the internal control system of Iranian banks. Journal of Financial Accounting Research, 14(1), 81-108.

Mukherjee, K. K., Reka, L., Mullahi, R., Jani, K., & Taraj, J. (2021). Public services: A standard process model following a structured process redesign. Business Process Management Journal, 27(3), 796-835. https://doi.org/10.1108/BPMJ-03-2020-0107

Omidvari, R. (2021). Investigating risk-based internal auditing and internal audit involvement in enterprise risk management: A case study of companies listed on the Tehran Stock Exchange. Quarterly Journal of Modern Research Approaches in Economic Management (Sustainable Growth and Development), 16(3), 47-66.

Polizzi, S., & Scannella, E. (2023). Continuous auditing in public sector and central banks: A framework to tackle implementation challenges. Journal of Financial Regulation and Compliance, 31(1), 40-59. https://doi.org/10.1108/JFRC-02-2022-0011

Pourahmadi, M. H., & Farsad Amanollahi, G. (2021). The effect of enterprise risk management on the relationship between external financing and earnings management. Quarterly Journal of Financial Accounting and Auditing Research, 13(49), 73-95.

Rabiei, K., & Fotouhi Fashtami, H. (2025). Investigating the Nonlinear Impact of Earnings Management and Business Strategy on Corporate Bankruptcy Risk Using the Generalized Method of Moments (GMM). Management Accounting and Auditing Knowledge, 14(56), 183-192. https://www.jmaak.ir/article_23510.html?lang=en

Ramezani, H. R., Azinfar, K., Gholamnia Roshan, H. R., & Fallah, R. (2022). The role of Islamic culture and auditor experience in the relationship between mutual fairness and audit quality in the environmental conditions of Iran. Civilica.

Sadati Tilehboni, S. V., Zabihi, A., & Khalili, Y. (2022). Investigating the effect of unsystematic risk on earnings management. Quarterly Journal of Accounting and Auditing Research, 53, 175-190.

Sajjadi, S. H., & Hooshmand Kashani, A. (2024). Using continuous auditing information in risk-based internal audit planning: A survey of internal audit managers and experts. Professional Auditing Research, 5(17), 114-143. https://doi.org/10.22034/jpar.2024.2034562.1329

Shams, E., & Rahimpour, M. (2022). The role of risk management and its evaluation in the performance of insurance companies. 14th National Conference on Economics, Management and Accounting, Shirvan, North Khorasan, Iran.

Shirbandi, H., Khalvati, S., & Farmani, A. (2023). The impact of liquidity flow risk management on financial stability. Shabak Specialized Scientific Journal, 9(1), 141-154.

Vaghfi, S. H., Hosseini, S. E., & Keshvari, F. (2022). The effect of cost leadership and differentiation strategies on firm risk emphasizing the role of risk management and intellectual capital. Commercial Research Quarterly, 104, 157-180.

Vakilzadeh Rouhalamini, M., Azadi, K., & Mohammadi Nodeh, F. (2024). Evaluating the factors affecting audit risk based on factor analysis approach. Management Accounting and Auditing Knowledge, 15(58), 197-216.

Downloads

Additional Files

Publication Timeline

- Submitted

- Revised

- Accepted