The Effect of Similarity Bias on Auditor Professional Judgment with Emphasis on the Moderating Role of Self-Esteem

DOI:

https://doi.org/10.61838/Keywords:

Similarity bias, self-esteem, auditor professional judgment, cognitive bias, audit quality, behavioral auditingAbstract

Objective: The present study aimed to investigate the effect of similarity bias on auditors’ professional judgment and to examine the moderating role of self-esteem in this relationship.

Methods and Materials: This study was applied research in terms of purpose and descriptive-survey research in terms of data collection method. The statistical population consisted of auditors employed by the Audit Organization and audit firms affiliated with the Iranian Association of Certified Public Accountants. Based on the Krejcie and Morgan sampling table, 139 auditors were selected as the study sample. Data were collected using standardized questionnaires related to similarity bias, auditor professional judgment, and self-esteem. Similarity bias was examined through two questionnaires distributed with a one-month interval, differing only in the similarity-bias scenario. Auditor professional judgment was measured using the Jenkins and Haynes questionnaire utilized in the study by Puspa (2008), while self-esteem was measured using the Rosenberg Self-Esteem Scale. Data analysis was performed using descriptive and inferential statistics, including Cronbach’s alpha reliability analysis, AVE and HTMT validity tests, Kolmogorov–Smirnov normality testing, and structural equation modeling for hypothesis testing.

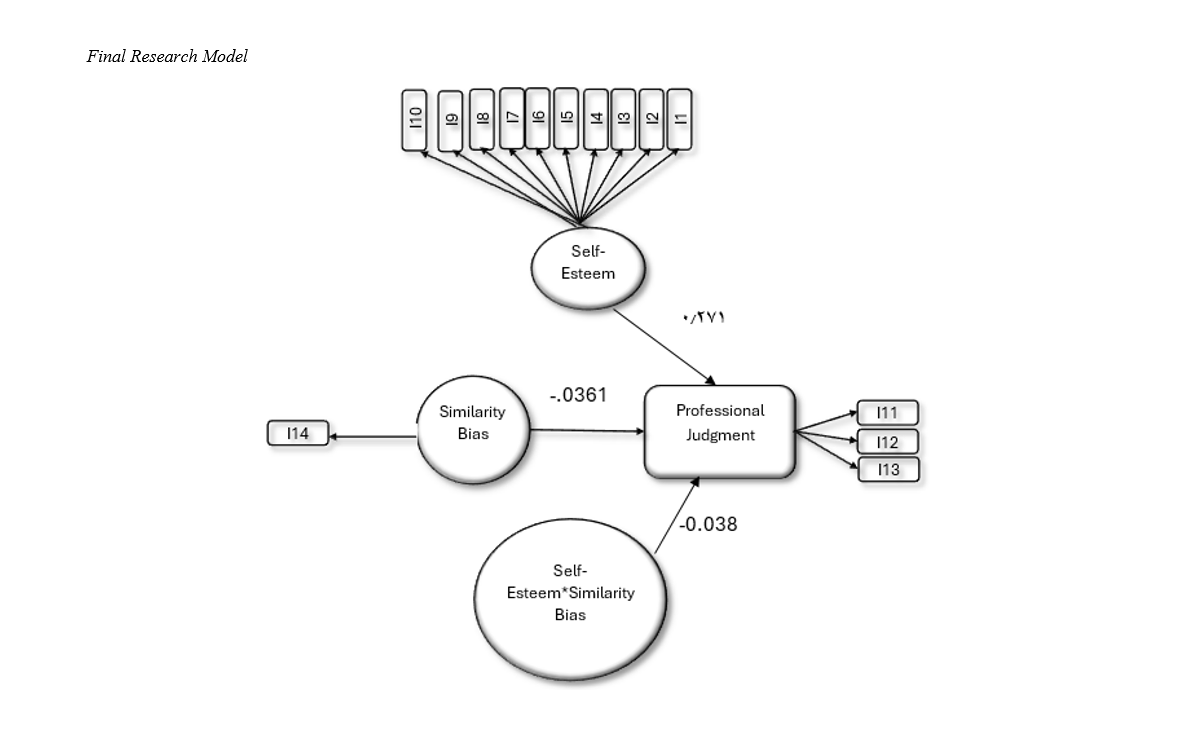

Findings: The findings demonstrated that similarity bias had a significant negative effect on auditors’ professional judgment (β = -0.361, t = 4.574, p < 0.001), indicating that increased similarity bias reduces the quality and objectivity of professional judgment. In contrast, self-esteem had a significant positive effect on auditor professional judgment (β = 0.271, t = 3.435, p = 0.001), suggesting that auditors with higher self-esteem demonstrate more accurate and confident professional judgments. However, the moderating effect of self-esteem on the relationship between similarity bias and auditor professional judgment was not statistically significant (β = -0.038, t = 0.822, p = 0.411). Therefore, the moderating hypothesis was rejected.

Conclusion: The results indicate that cognitive biases, particularly similarity bias, can significantly impair auditors’ professional judgment and potentially threaten audit quality and objectivity. At the same time, self-esteem contributes positively to auditors’ decision-making quality and professional confidence.

Downloads

References

Aghaei Chadgani, A., Rezaei, M., & Kamali, E. (2024). The Effect of Auditors' Self-Efficacy and Audit Firm Size on Auditors' Judgment and Decision-Making. Judgment and Decision-Making in Accounting, 3(2), 145-165.

Arefmanesh, Z., & Safari, H. (2025). The Impact of Psychological Capital and Auditors' Experience on the Quality of Judgment and Professional Decision-Making. Professional Auditing Research(18), 179-196. https://www.sid.ir/paper/1522135/fa

Becker, J., Medjedovic, J., & Merkle, C. (2019). The Effect of CEO Extraversion on Analyst Forecasts: Stereotypes and Similarity Bias. Financial Review, 54(1), 133-164.

Behzadian, F., & Izadi Nia, N. (2017). An Investigation of Expectation Gap Between Independent Auditors and Users from Auditing Services Related to the Quality of Auditing Services Based on Their Role and Professional Features in Auditing Process.

Brown, V. L., Dickins, D., Hermanson, D., Higgs, J., Jenkins, J. G., & Nolder, C. J. (2019). Comments of the Auditing Standards Committee of the Auditing Section of the American Accounting Association on Proposed Statement on Auditing Standards (SAS), Audit Evidence. Current Issues in Auditing.

Dewi, P. P., & Dwiyanti, K. (2018). Professional Commitment, Self-Efficacy and Ethical Decision Auditor.

Djaddang, S., Lyshandra, S., Wulandjani, H., & Sulistiawarni, E. (2018). The Relationship Between Self-Efficacy Towards Audit Quality with Individualism Culture as Mediates: Evidence from Indonesia.

Dong, L., Sarikas, R., & Djatej, A. (2019). Partner Rotation or Extended Rotations? The Effect of Confirmation Bias and Motivated Reasoning Bias on Objectivity and Independence: A Framework. Journal of Global Business Insights.

Fanani, F., Prastika, S., Agustin, T., & Rahman, T. I. M. (2024). The Moderating Effect of Interpersonal Conflict in Knowledge Sharing and Ego Depletion on Auditor's Judgment and Decision-Making Quality Relationship. MANAGEMENT AND ACCOUNTING REVIEW.

Ghadimi, F., Ali Ahmadi, S., & Alimoradi, M. (2024). The Moderating Role of Stereotype Bias and Similarity Bias in the Effect of CEO Extraversion on Financial Analysts' Forecasts. Journal of Accounting Knowledge, 16(3), 121-138.

Gwala, M., & Nomlala, B. (2021). Mandatory Audit Firm Rotation: A Student Perspective; An Assessment of the Perceived Impact on Auditor Independence. Jurnal Akuntansi & Auditing Indonesia.

H, A., M, A., & Kusumawati, A. (2018). The Effect of Self-Efficacy and Obedience Pressure on Audit Judgment by Using Task Complexity and Moral Reasoning as the Moderating Variable. International Journal of Advanced Research.

Hasibuan, A. K. F., Bukit, R. B., & Rini, E. S. (2022). The Effect of Framing, Halo Effect and Auditors Experience on Audit Judgement: Study on Auditors Public Accountant Office (KAP) in Medan City. International Journal of Research and Review, 9(9), 37-47.

Heidari, Z., & Mashayekh, S. (2025). The Consequences of Disclosing Key Audit Matters on Investor Judgment and Decision-Making. Empirical Accounting Research, 15(1), 53-84.

Henrizi, P., Himmelsbach, D., & Hunziker, S. (2021). Anchoring and Adjustment Effects on Audit Judgments: Experimental Evidence from Switzerland. Journal of Applied Accounting Research, 22(4), 598-621.

Hotbin, H. (2022). The Effect of Auditor Competence, Skepticism, Self-Esteem, Role Conflict, and Religiosity on Audit Quality. International Journal of Contemporary Accounting, 4(1), 1-20.

Jannati, S., Kumar, A., Niessen-Ruenzi, A., & Wolfers, J. (2023). In-Group Bias in Financial Markets. SSRN. https://doi.org/10.2139/ssrn.2884218

Kamal, C. N. P. (2023). Auditor Independence and Its Influence on Accounting Behavior: A Systematic Literature Review. Journal Integration of Management Studies.

Kohandel, Z., & Doaei, M. (2023). The Role of Emotional Biases of Status Quo Bias, Loss Aversion, Representativeness Bias, and Cognitive Dissonance Bias in Auditors' Mistakes. Accounting and Auditing Research, 15(58), 199-218.

Larasati, B., & Fatima, E. (2024). Evaluation of the Impact of Hybrid Working on Auditors' Self-Efficacy. East Asian Journal of Multidisciplinary Research.

Lee, S.-c., Su, J.-M., Tsai, S., Lu, T.-L., & Dong, W. (2016). A Comprehensive Survey of Government Auditors' Self-Efficacy and Professional Development for Improving Audit Quality. SpringerPlus.

Maradona, A. F. (2020). A Qualitative Exploration of Heuristics and Cognitive Biases in Auditor Judgements.

Merawati, L. K. (2019). Determinant of Auditor's Performance: Case of Government Auditor in Bali Province.

Munoz-Izquierdo, N., Camacho-Minano, M., Sanchez-Martin, M.-d.-P., & Pascual-Ezama, D. (2024). Is Auditor Financial Decision-Making Affected by Prior Audit Report Information? A Behavioral Approach.

Razali, F. M. (2020). Examining Types of Audit Judgment and Objectivity Threat: Empirical Findings from Public and Private Sector Internal Auditors in Malaysia.

Rustan, R. (2021). Several Factors Affecting Audit Judgment with Moral Reasoning Moderation. ATESTASI: Jurnal Ilmiah Akuntansi.

Sabilillah, R., Hardi, H., & Safitri, D. (2024). Examining the Locus of Control, Auditor Experience, Self-Efficacy and Task Complexity for Audit Judgment. Studi Akuntansi dan Keuangan Indonesia.

Sambara, E. J., Asnawi, M., & Daat, S. C. (2021). The Impact of the Auditor's Personal Characteristics Through Dysfunctional Audit Behaviour Acceptance Towards the Audit Quality. Jurnal Akuntansi, Audit, dan Aset.

Silva, R., Costa, P., & Oliveira, L. (2025). The Auditing Profession and Artificial Intelligence: A Focus on Human Judgment and Accountability. Journal of Business Ethics, 186, 345-367.

Su, J.-M., Lee, S.-c., Tsai, S., & Lu, T.-L. (2016). A Comprehensive Survey of the Relationship Between Self-Efficacy and Performance for Governmental Auditors. SpringerPlus.

Tabesh, Z., Abdoli, M. R., & Yavarpour, H. (2020). Examining the Halo Effect on the Auditor's Professional Career. Accounting and Auditing Research, 12(45), 89-112.

Tanone, J., & Harindahyani, S. (2018). The Impact of Heuristics and Biases in the Application of Professional Judgement by Internal Auditors in the Stage of Fieldwork.

Williams, J. (2024). The Impact of Cognitive Biases on Auditors' Judgment. International Journal of Auditing, 21(3), 154-179.

Yasa, I. B. A., Sukayasa, I. K., & Pratiwi, N. (2019). The Role of Self-Efficacy Mediating the Effect of Goal Orientation and Task Complexity on Judgment Audit Performance. Proceedings of the International Conference on Applied Science and Technology 2019 - Social Sciences Track (iCASTSS 2019),

Zolkaflil, S., Nazri, S. N. F. S. M., Razali, F. M., Tarmizi, M. A., & Masum, M. H. (2023). Money Laundering Framework for Professional Accountants: Post COVID-19. Journal of Nusantara Studies (JONUS).

Downloads

Additional Files

Publication Timeline

- Submitted

- Revised

- Accepted