An Analytical Approach to the Function of Internal Auditors’ Job Well-Being in Auditor Professional Maturity

DOI:

https://doi.org/10.61838/kman.ijimob.5101Keywords:

Occupational well-being of internal auditors, auditor's professional maturity, structural factors, environmental factorsAbstract

Objective: The objective of this study was to develop and validate a comprehensive model of internal auditors’ job well-being and examine its effect on auditor professional maturity.

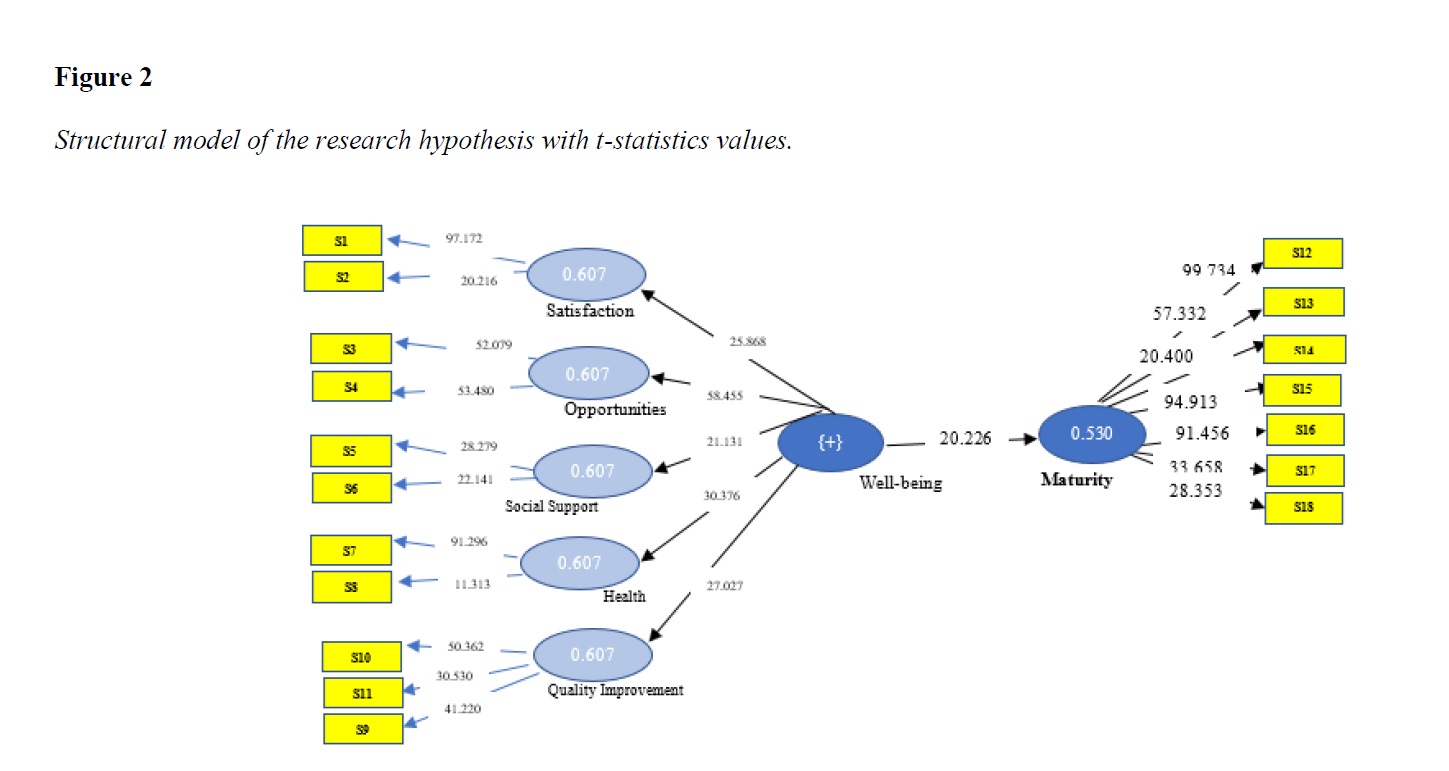

Methods and Materials: This research adopted a mixed-methods design combining qualitative and quantitative approaches. In the qualitative phase, thematic analysis was conducted through semi-structured interviews with expert internal auditors and academic specialists to identify the underlying dimensions of internal auditors’ job well-being. Extracted themes were categorized into overarching, organizing, and basic themes, forming the conceptual framework of the model. In the quantitative phase, data were collected using a researcher-developed questionnaire measuring job well-being dimensions and a standardized instrument assessing auditor professional maturity. The statistical population consisted of internal auditors, and sampling was conducted using purposive selection in the qualitative phase and survey-based sampling in the quantitative phase. The Delphi technique was employed to confirm content validity and expert consensus regarding identified components. Measurement model reliability and validity were evaluated using confirmatory factor analysis, Cronbach’s alpha, composite reliability, convergent validity (AVE), and discriminant validity (Fornell–Larcker criterion). Structural Equation Modeling based on the Partial Least Squares (PLS-SEM) approach was applied to test the research hypothesis and assess model fit.

Findings: The structural model demonstrated satisfactory measurement and structural fit indices. Results indicated that internal auditors’ job well-being has a positive and statistically significant effect on auditor professional maturity (β = 0.564, T = 20.226). The model explained approximately 52.9% of the variance in professional maturity. All dimensions of job well-being—including professional satisfaction, growth and development opportunities, social support and communication, psychological and physical health, and enhancement of audit process quality—were validated and significantly contributed to the latent construct of job well-being. Reliability, convergent validity, discriminant validity, and predictive relevance indices confirmed the robustness of the proposed model.

Conclusion: The findings indicate that internal auditors’ job well-being functions as a fundamental driver of professional maturity by strengthening psychological readiness, ethical judgment, professional competence, and organizational engagement. Promoting well-being-oriented organizational environments can enhance audit effectiveness, reinforce professional independence, and improve governance quality. The study highlights the strategic importance of integrating human-centered well-being policies into professional auditing frameworks to achieve sustainable professional development.

Downloads

References

Abbasi Estamal, M. R., & Marefat, M. (2022). Investigating the effect of auditors' professional maturity and job satisfaction on organizational commitment. Ethics and Behavior Studies in Accounting and Auditing, 3(1), 65-84. https://sebaa.qom.iau.ir/article_691259.html?lang=en

Abolghasemi, M., Abdoli, M. R., Valiyan, H., & Dehdar, F. (2021). Designing a model of contextual causes for the development of auditors' professional maturity based on the grounded theory approach. Empirical Research in Accounting, 11(39), 105-136. https://jera.alzahra.ac.ir/article_5327.html?lang=fa

Arefmanesh, Z., & Saffari, H. (2024). The effect of auditors' psychological capital and experience on professional judgment and decision-making quality: The moderating role of professional skepticism. Professional Auditing Research, 5(18), 108-133. https://www.sid.ir/paper/1522135/fa

Bairami, L., Jahangirnia, H., Banimahd, B., Izadpour, M., & Moghadam, H. (2025). The effect of auditor self-efficacy on fraud risk assessment with the mediating role of auditors' fundamental and developed creativity. Journal of Management Accounting and Auditing Knowledge, 14(54), 239-250. https://www.jmaak.ir/article_23574.html

Barker, P., Monks, K., & Buckley, F. (1999). The role of mentoring in the career progression of chartered accountants. The British Accounting Review, 31(3), 297-312. https://doi.org/10.1006/bare.1999.0103

Castka, P., Zhao, X., Bremer, P., Wood, L. C., & Mirosa, M. (2021). Supplier audits during COVID-19: A process perspective on their transformation and implications for the future. The International Journal of Logistics Management. https://doi.org/10.1108/IJLM-05-2021-0302

Chen, Y., Li, S., Xia, Q., & He, C. (2017). The relationship between job demands and employees' counterproductive work behaviors: The mediating effect of psychological detachment and job anxiety. Frontiers in psychology, 8(4), 1890-1898. https://doi.org/10.3389/fpsyg.2017.01890

Chen, Y. H., Wang, K. J., & Liu, S. H. (2023). How personality traits and professional skepticism affect auditor quality? A quantitative model. Sustainability, 15(7), 74-93. https://doi.org/10.3390/su15021547

Curtis, B., Hefley, B., & Miller, S. (2018). People Capability Maturity Model (PCMM) Version 2.0 (2nd ed.). Carnegie Mellon University. https://apps.dtic.mil/sti/html/tr/ADA395316/

Diaz, M. C., Loraas, T. M., & Apostolou, B. (2017). How do mentoring rewards influence experienced auditors? The British Accounting Review. https://doi.org/10.1016/j.bar.2017.09.009

Griffith, E. E., Hammersley, J. S., & Hickey, A. S. (2025). "A Fly on the Wall": Promoting auditors' observational learning with cognitive process modeling and learning climate. https://doi.org/10.2139/ssrn.5200422

Hendar, F., & Harahap, D. (2023). The influence of time budget pressure, auditor experience, and auditor competence on audit judgment. Kajian Akuntansi, 24(8), 374-387. https://doi.org/10.29313/kajian_akuntansi.v24i2.2671

Hooshmand Naqabi, Z., Shahbazi, A., & Abbasabadi Arabi, F. (2023). The impact of auditors' social and human capital on audit services. Financial Economics, 3(64), 1-18. https://www.sid.ir/paper/1097924/fa

Kadkhodaei Eliaderani, M., & Banimahd, B. (2021). The relationship between value orientation, positive emotions and perception of fairness with internal auditors' inclination to fraud reporting. Journal of Value and Behavioral Accounting, 6(11), 67-91. https://aapc.khu.ac.ir/browse.php?a_code=A-10-50-2&sid=1&slc_lang=fa

Khanmohammadi, M., Moradi, M., & Nargesian, A. (2025). Key themes of ambiguity, duality and role conflict affecting the distortion of internal audit independence: A thematic analysis study. Journal of Value and Behavioral Accounting, 10(19), 1-21. https://aapc.khu.ac.ir/browse.php?a_id=1348&sid=1&slc_lang=fa

Kun, A., & Gadanecz, P. (2022). Workplace happiness, well-being and their relationship with psychological capital: A study of Hungarian teachers. Current Psychology, 41(1), 185-199. https://doi.org/10.1007/s12144-019-00550-0

McCarthy, S. (2018). Financial Management Maturity Model: A Good Practice Guide. https://www.audit.gov.ie/en/find-report/publications/2018/special-report-101-financial-management-maturity-model-a-good-practice-guide.pdf

Molina-Sánchez, H., Ariza-Montes, A., Ortiz-Gómez, M., & Leal-Rodríguez, A. (2019). The subjective well-being challenge in the accounting profession: The role of job resources. International journal of environmental research and public health, 16(17), 3073. https://doi.org/10.3390/ijerph16173073

Munidewi, I. A. B., Ludigdo, U., Djamhuri, A., & Andayani, W. (2024). Role of affective neuroscience in audit judgement and decision making: A systematic literature review for auditing research. Australasian Accounting, Business and Finance Journal, 18(1), 130-147. https://doi.org/10.14453/aabfj.v18i1.08

Muterera, J., & Brettle, J. A. (2024). Exploring the impact of auditor well-being on audit quality. International journal of management, accounting & economics, 11(3). https://www.researchgate.net/profile/Jonathan-Muterera/publication/379778607_Exploring_the_Impact_of_Auditor_Well-Being_on_Audit_Quality/links/6619977339e7641c0bbb01a2/Exploring-the-Impact-of-Auditor-Well-Being-on-Audit-Quality.pdf

Payne, S. C., & Huffman, A. H. (2005). A longitudinal examination of the influence of mentoring on organizational commitment and turnover. Academy of Management journal, 48(1), 158-168. https://doi.org/10.5465/amj.2005.15993166

Ponomareva, Y., Uman, T., Broberg, P., Vinberg, E., & Karlsson, K. (2020). Commercialization of audit firms and auditors' subjective well-being. Meditari Accountancy Research, 28(4), 565-585. https://doi.org/10.1108/MEDAR-10-2018-0384

Rottinghaus, P. J., Day, S. X., & Borgen, F. H. (2005). The Career Futures Inventory: A measure of career-related adaptability and optimism. Journal of Career Assessment, 13(1), 3-24. https://doi.org/10.1177/1069072704270271

Russell, J. E. A. (2008). Promoting subjective well-being at work. Journal of Career Assessment, 16(1), 117-131. https://doi.org/10.1177/1069072707308142

Safarzadeh, M. H., Asna Ashari, H., & Gazderazi, J. (2024). Auditors' subjective well-being: Evidence from the role of audit firms' commercialization with an emphasis on auditor characteristics. Journal of Value and Behavioral Accounting, 9(17), 97-151. https://aapc.khu.ac.ir/browse.php?a_id=1235&sid=1&slc_lang=fa

Seyednejad Fahim, S. R., & Hosseinnia Dilman, K. (2023). An analysis on the psychological well-being of public sector accountants based on self-determination theory; Exploring the role of positive affect and psychological safety. Journal of Value and Behavioral Accounting, 8(16), 211-238. https://aapc.khu.ac.ir/browse.php?a_id=1229&sid=1&slc_lang=fa&ftxt=0

Summers, E. M., Morris, R. C., Bhutani, G. E., Rao, A. S., & Clarke, J. C. (2021). A survey of psychological practitioner workplace well-being. Clinical Psychology & Psychotherapy, 28(2), 438-451. https://doi.org/10.1002/cpp.2509

Tajik Jalayeri, M., Ramezani, J., & Kamyabi, Y. (2022). The effect of the international professional practices framework on internal audit effectiveness. Financial Accounting and Auditing Research, 14(53), 77-102. https://www.sid.ir/paper/964802/fa

Tuan Mansor, T. M., Mohamad Ariff, A., Hashim, H. A., & Ngah, A. H. (2021). External whistleblowing intentions of auditors: A perspective based on stimulus-organism-response theory. Corporate Governance. https://doi.org/10.1108/CG-03-2021-0116

Umans, T., Broberg, P., Schmidt, M., Nilsson, S., & Olsson, E. (2016). Feeling well by being together: Study of Swedish auditors. Work, 54(1), 79-86. https://doi.org/10.3233/WOR-162270

Vaz, C. R., Selig, P. M., & Viegas, C. V. (2018). A proposal of intellectual capital maturity model (ICMM) evaluation. Journal of Intellectual Capital. https://doi.org/10.1108/JIC-12-2016-0130

Zhang, L., & Guo, C. (2024). Can corporate ESG performance improve audit efficiency? Empirical evidence based on audit latency perspective. PLoS One, 19(3), e0299184. https://doi.org/10.1371/journal.pone.0299184

Downloads

Additional Files

Publication Timeline

- Submitted

- Revised

- Accepted