A Structural Model Based on the Relationship Between Auditors’ Dark Personality Traits and Judgment Regarding Key Audit Matters

DOI:

https://doi.org/10.61838/Keywords:

dark personality traits, key audit matters, auditor judgmentAbstract

Objective: The present study aimed to investigate the effect of auditors’ dark personality traits on professional judgment regarding Key Audit Matters (KAMs).

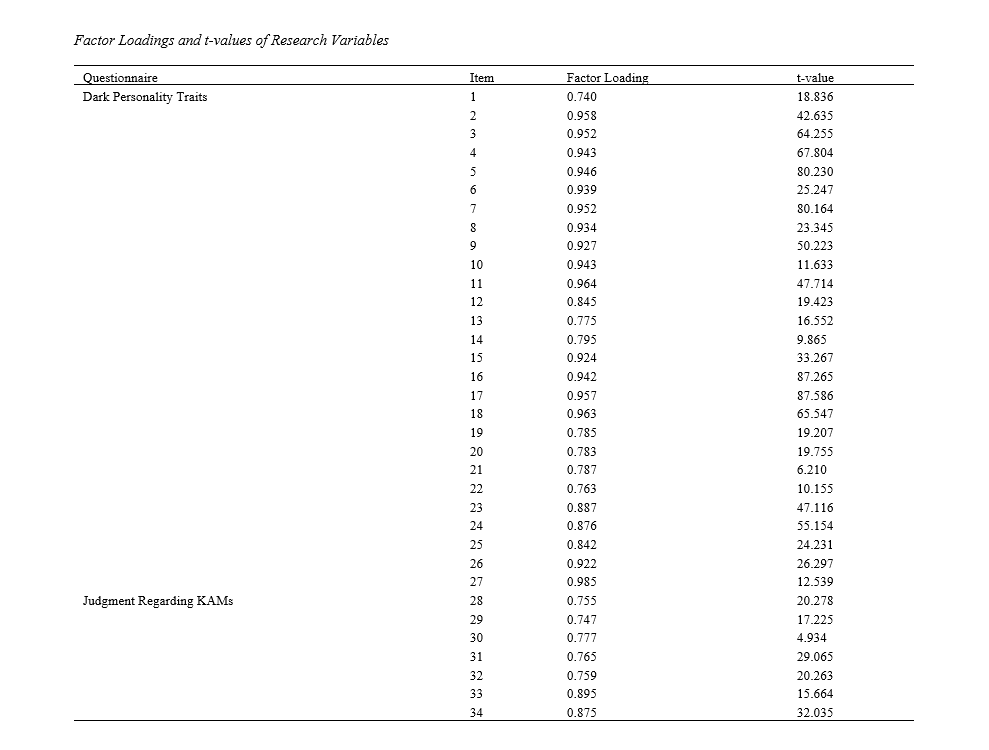

Methods and Materials: This study was applied in terms of purpose and descriptive–correlational in terms of methodology. The statistical population consisted of all certified public accountants who were members of the Iranian Association of Certified Public Accountants and the Audit Organization in 2026. Based on Cochran’s formula, the estimated sample size was 384 participants; however, due to incomplete questionnaire returns, 237 usable questionnaires were ultimately collected through convenience and snowball sampling methods. Data were gathered using the Dark Personality Traits Questionnaire developed by Jones and Paulhus (2014) and a questionnaire assessing judgment regarding Key Audit Matters adapted from prior auditing studies. Data analysis was conducted using Partial Least Squares Structural Equation Modeling (PLS-SEM). Reliability and validity of the instruments were confirmed through Cronbach’s alpha, composite reliability, Average Variance Extracted (AVE), and confirmatory factor analysis.

Findings: The results indicated that all factor loadings exceeded the acceptable threshold of 0.40 and all t-values were greater than 1.96, confirming the convergent validity of the measurement model. Cronbach’s alpha and composite reliability coefficients for all constructs exceeded 0.90, demonstrating strong internal consistency. The coefficient of determination (R²) for auditors’ judgment regarding KAMs was 0.572, indicating that dark personality traits explained 57.2% of the variance in professional judgment. Furthermore, the Goodness-of-Fit (GOF) index was 0.613, confirming strong overall model fit. Hypothesis testing revealed that dark personality traits had a significant negative effect on auditors’ judgment regarding KAMs (β = -0.552, t = 3.622, p < 0.001).

Conclusion: The findings demonstrate that auditors’ dark personality traits significantly impair professional judgment regarding Key Audit Matters. The results highlight the importance of behavioral and psychological factors in audit quality and suggest that personality characteristics may influence auditors’ objectivity, skepticism, and ethical decision-making processes. The study contributes to the interdisciplinary literature linking auditing and psychology and provides practical implications for audit firms and regulatory bodies in identifying behavioral risks and strengthening professional judgment quality through appropriate control and training mechanisms.

Downloads

References

Asare, S. K., & Wright, A. M. (2012). Investors’, Auditors’, and Lenders’ Understanding of the Message Conveyed by the Standard Audit Report on the Financial Statements. Accounting Horizons, 26(2), 193-217.

Bhaskar, L. S., Majors, T. M., & Vitalis, A. (2019). Are Auditor Negotiations Impaired during Depleting Times? The Importance of Client Characteristics and Auditor Skepticism. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3373379

Bonner, S. E. (2008). Judgment and Decision Making in Accounting. Prentice Hall.

Cameran, M., & Campa, D. (2023). Key Audit Matters and Audit Outcomes: Evidence from the European Union. SSRN.

D’Souza, M. F., Aragão, I. R., & De Luca, M. M. M. (2018). Analysis of the Occurrence of Machiavellianism and Narcissism in the Discourse in Management Reports of Companies Involved in Financial Scandals. Revista de Educação e Pesquisa em Contabilidade. https://doi.org/10.17524/repec.v12i3.1899

D’Souza, M. F., & Lima, G. A. S. F. (2015). The Dark Side of Power: The Dark Triad in Opportunistic Decision-Making. Advances in Scientific and Applied Accounting, 8(2), 135-156. https://doi.org/10.2139/ssrn.2641799

D’Souza, M. F., & Lima, G. A. S. F. (2019). A Look at Dark Triad Traits and Cultural Values of Accounting Students. Advances in Scientific and Applied Accounting, 1(1), 161-183. https://doi.org/10.14392/ASAA.2019120109

Ecim, D., Maroun, W., & Duboisee de Ricquebourg, A. (2023). An Analysis of Key Audit Matter Disclosures in South African Audit Reports from 2017 to 2020. South African Journal of Business Management, 54(1), 3669.

Góis, A. D., Lima, G. A. S. F., De Luca, M. M. M., & Gotti, G. (2024). Dark Tetrad Personality and Earnings Management: The Moderating Effect of Corporate Reputation. Advances in Scientific and Applied Accounting, 17(2), 209-226. https://doi.org/10.14392/asaa.2024170209

Goudarzi, S., Hemmatfar, M., & Janani, M. H. (2025). A model for identifying the personality and ethical characteristics of independent auditors in the country. Management Accounting and Auditing Knowledge, 14(56), 383-394.

Heilmann, A. G. M. (2019). The Consequences of Disclosing Key Audit Matters (KAMs): A Review of the Academic Literature. Maandblad voor Accountancy en Bedrijfseconomie, 93, 5-14. https://doi.org/10.5117/mab.93.29496

Hobson, J. L., Stern, M. T., & Zimbelman, A. F. (2020). The Benefit of Mean Auditors: The Influence of Social Interaction and the Dark Triad on Unjustified Auditor Trust. Contemporary Accounting Research, 37(2), 1217-1247. https://doi.org/10.1111/1911-3846.12511

Janrosl, V. S. E., Muda, I., Sadalia, I., & Nasution, A. A. (2025). Fraud detection mediation: Personality auditor and forensic accounting on audit quality. International Journal of Accounting, Economics, Finance, & Accounting, 21(2), 190-212.

Jones, D. N., & Paulhus, D. L. (2017). Duplicity among the Dark Triad: Three Faces of Deceit. Journal of personality and social psychology, 113(2), 329-342. https://doi.org/10.1037/pspp0000139

Majors, T. M. (2015). The Interaction of Communicating Measurement Uncertainty and the Dark Triad on Managers’ Reporting Decisions. The Accounting Review, 91(3), 973-992. https://doi.org/10.2308/accr-51276

Marçal, R. R., & Alberton, L. (2020). Relationship between Dark Personality Traits and Professional Skepticism of Independent Auditors. Revista de Educação e Pesquisa em Contabilidade, 14(4). https://doi.org/10.17524/repec.v14i4.2663

Nelson, M., & Tan, H. T. (2005). Judgment and Decision Making Research in Auditing: A Task, Person, and Interpersonal Interaction Perspective. Auditing: A Journal of Practice & Theory, 24(1), 41-71. https://doi.org/10.2139/ssrn.761706

Olsen, K. J., & Stekelberg, J. M. (2016). CEO Narcissism and Corporate Tax Sheltering. The Journal of the American Taxation Association, 38(1), 1-22. https://doi.org/10.2308/atax-51251

Pinto, I., & Morais, A. I. (2019). What Matters in Disclosures of Key Audit Matters: Evidence from Europe. Journal of International Financial Management & Accounting, 30(2), 145-162.

Rosequist, R., & Kromka, S. M. (2024). The Dark Side of Conflict: The Relationships between Dark Tetrad Personality Traits and Conflict Management Styles. Imagination, Cognition and Personality, 44(2), 121-141. https://doi.org/10.1177/02762366241281253

Schluetera, J. K. M., & Sakela, V. S. R. (2022). Dark Triad Personality Traits and Auditor Independence: A Systematic Literature Review. SSRN, 42. https://doi.org/10.2139/ssrn.4014690

Segal, M. (2019). Key Audit Matters: Insight from Audit Experts. Meditari Accountancy Research, 27(3), 472-494.

Silva, A., Cunha, P. R., & D’Souza, M. F. (2020). Influence of Executives’ Dark Tetrad on Earnings Management. 20th USP International Conference in Accounting, São Paulo, SP.

Spain, S. M., Harms, P. D., & Lebreton, J. M. (2014). The Dark Side of Personality at Work. Journal of Organizational Behavior, 35(1), 41-60. https://doi.org/10.1002/job.1894

Zaki, M., & Elfar, E. (2023). The Impact of Partner Perfectionism on Audit Quality: The Mediating Role of Professional Skepticism in the Egyptian Context. Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-06-2023-0296

Zolfi, S., & Yazdanian, N. (2024). Dark Personality Traits of Auditors and Their Effect on Fraud Risk Assessment. Accounting and Auditing Research, 15(57), 179-206.

Downloads

Additional Files

Publication Timeline

- Submitted

- Revised

- Accepted