Identification of Practical Indicators for Social Auditing in Loan Disbursement in Banks and Its Impact on Reducing Social Financial Crises in Society

Keywords:

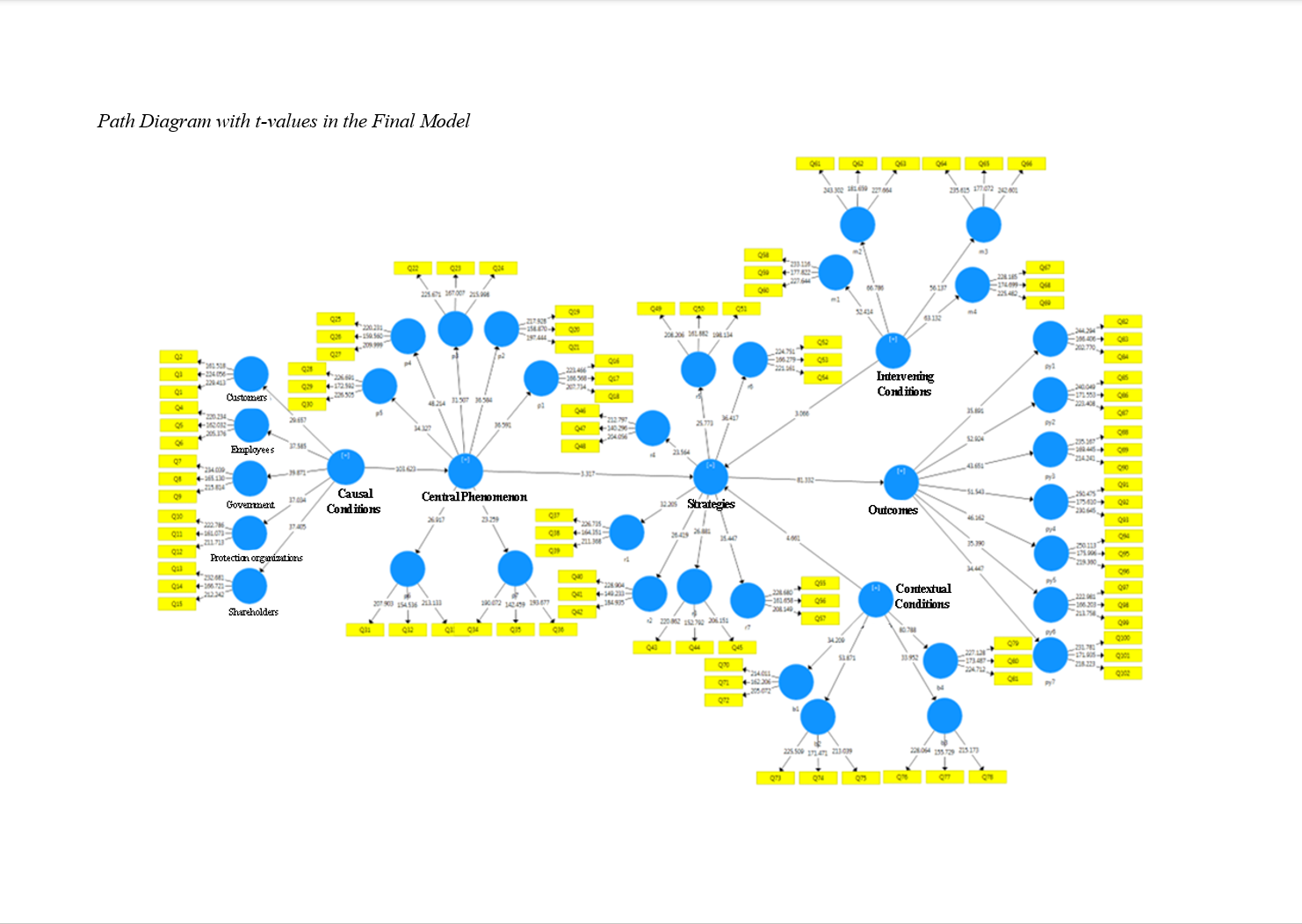

Social auditing of banking activities, social financial crises, grounded theoryAbstract

Objective: The aim of this study is to explore green research and development (R&D) in the home appliance industry.

Methods and Materials: This research is applied in nature, and the data collection method is descriptive-survey. Initially, by reviewing the literature and using qualitative content analysis, 30 factors were extracted as indicators for green development and formulation, categorized into five dimensions: green management, product and stakeholder performance, internal environment management, green innovation, and energy and resource consumption management. In the second stage, the fuzzy Delphi technique was employed, with a two-stage survey conducted among 15 experts selected through purposive sampling to achieve group consensus and filter the findings from the first stage. Finally, to assess the opinions of employees in the home appliance industry regarding green R&D indicators, a questionnaire was distributed among 170 employees, selected through Cochran’s formula and simple random sampling. The results were analyzed using SPSS software and a one-sample t-test.

Findings: The findings showed that all these indicators were significantly identified as green R&D indicators in the home appliance industry at a 95% confidence level. Based on the results, the product design improvement indicator, with an average score of (4.18), received the highest rating from employees. This was followed by access to new markets and customers with an average score of (4.14), a green image of the company with an average score of (4.11), green product innovation with an average score of (4.10), and enhancing the company's green position with an average score of (4.02), respectively.

Conclusion: The findings highlight the significance of improving product design, accessing new markets, and promoting a green company image as crucial factors for achieving sustainable development.

Downloads

References

Amran, A., & Fauzi, H. (2017). Social responsibility disclosure in Islamic banks: A comparative study of Indonesia and Malaysia. Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-01-2015-0016

Batra, G. S. (1996). Dynamics of social auditing in corporate enterprises; A study of the Indian corporate sector. Managerial Auditing Journal, 11(2), 36-45. https://doi.org/10.1108/02686909610107960

Bayat, A., & Ali-Ahmadi, S. (2014). Audit Delay and Timeliness of Financial Reporting. Financial Accounting and Auditing Research, 6(22), 97-121. https://journals.iau.ir/article_510516_883182db14d0145dfe8fcf99188e3657.pdf

Belasri, S., Gomes, M., & Pijourlet, G. (2020). Corporate social responsibility and bank efficiency. Journal of Multinational Financial Management, 54. https://doi.org/10.1016/j.mulfin.2020.100612

Breton, J. R. (2000). World affairs social audit. worldaffairs.com/audit.htm

De Oliveira Santini, F., Lugo, D. B., Junior Ladeira, W., Akhtar, S., Rocha, L. d. S., & Sott, M. K. (2024). Corporate social responsibility as a moderator of loyalty antecedents in the Brazilian banking context. International Journal of Bank Marketing, ahead-of-print(ahead-of-print). https://doi.org/10.1108/IJBM-12-2023-0667

Eklund, M. A. (2024). The Determinants of Corporate Social Responsibility (CSR) Committee: Executive Compensation, CSR-based Incentives and ESG Performance. Social Responsibility Journal, 20(7), 1240-1255. https://doi.org/10.1108/srj-07-2022-0303

Fahreza, I. A. (2023). Does the Disclosure of Islamic Corporate Social Responsibility, Islamic Corporate Governance, Profitability, and Bank Size Affect Tax Avoidance in Islamic Commercial Banks in Indonesia? Ultimaccounting Jurnal Ilmu Akuntansi, 222-240. https://doi.org/10.31937/akuntansi.v15i2.3296

Hanić, A., & Smolo, E. (2022). Islamic Approach to Corporate Social Responsibility: An International Model for Islamic Banks. International Journal of Islamic and Middle Eastern Finance and Management, 16(1), 175-191. https://doi.org/10.1108/imefm-07-2021-0284

Pirayesh, R., & Salehi, R. (2018). The Effects and Functions of Corporate Governance and Social Responsibility in Financial Institutions and Banks. Journal of Research in Accounting and Economic Sciences, 2(1), 31-42. https://www.magiran.com/paper/1852646/%D8%A8%D8%B1%D8%B1%D8%B3%DB%8C-%D8%A7%D8%AB%D8%B1%D8%A7%D8%AA-%D9%88-%DA%A9%D8%A7%D8%B1%DA%A9%D8%B1%D8%AF%D9%87%D8%A7%DB%8C-%D8%AD%D8%A7%DA%A9%D9%85%DB%8C%D8%AA-%D8%B4%D8%B1%DA%A9%D8%AA%DB%8C-%D9%88-%D9%85%D8%B3%D8%A6%D9%88%D9%84%DB%8C%D8%AA-%D8%A7%D8%AC%D8%AA%D9%85%D8%A7%D8%B9%DB%8C-%D8%AF%D8%B1-%D9%85%D9%88%D8%B3%D8%B3%D8%A7%D8%AA-%D9%85%D8%A7%D9%84%DB%8C-%D9%88-%D8%A8%D8%A7%D9%86%DA%A9-%D9%87%D8%A7

Saberi, Z., & Samiei-Nasr, M. (2022). Enhancing Customer Loyalty: An Analysis of Bank Dey's Corporate Social Responsibility in Tehran. Quarterly Journal of New Research Approaches in Management and Accounting, 6(84), 1265-1279. https://majournal.ir/index.php/ma/article/view/1320/1079

Sulaeman, A. (2024). The Influence of Capital Intensity, Leverage, Profitability, and Corporate Social Responsibility on Tax Avoidance With Firm Size as a Moderating Variable. Asian Journal of Economics Business and Accounting, 24(5), 433-442. https://doi.org/10.9734/ajeba/2024/v24i51320

Wahdi, N. (2024). The Influence of Corporate Social Responsibility and Profitability on Tax Avoidance. Innovation Business Management and Accounting Journal, 3(1), 30-36. https://doi.org/10.56070/ibmaj.2024.004

Downloads

Additional Files

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2024 Mokhtar Felehgari (Author); Babak Jamshidinavid (Corresponding Author); Mehrdad Ghanbari , Forouzan Mohammadi Yarijani (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

How to Cite